A solid basis for the future

A solid basis for the future

DELA Natura- en levensverzekeringen N.V. (DELA Natura) is an international funeral insurer and part of Coöperatie DELA. We have been providing care and financial peace of mind around when a loved one passes away for nearly 90 years now. That is our core. It forms the basis on which we build our relationships with customers, suppliers, and partners. DELA Natura is active in three countries: the Netherlands, Belgium, and Germany.

We strive for an affordable and dignified funeral for everyone while keeping the cost of funerals and insurance premiums as low as possible. Inflation makes funerals more expensive every year, which has an impact on insurance premiums. Growth and efficient business operations have been key to achieving that since our very beginning. Growth gives us scale advantages, while continuous process improvement enables us to keep costs low and provide high-quality services.

With our collective purchasing power and by investing our premiums, we are able to inflation-proof our funeral insurance and keep increases in premium rates under control. It is not our goal to maximise profit: profit is a means to invest, grow, and strengthen our solid financial basis – to keep increases in premium rates under control and safeguard our future.

We always look to the long term because we also have financial obligations that need to be fulfilled in the distant future. We therefore continue adapting our products, services, and facilities to the changing requirements of customers and to trends in society. Customers are taking more charge of their choices and expect transparency about options and costs. Sustainability and community involvement are becoming increasingly important in the expectations of customers, employees, and partners. In addition, technology, data, and artificial intelligence are changing how we work as they contribute to transparency and remote collaboration and create opportunities for service innovation. Geopolitical tensions, economic uncertainty, and changing laws and regulations make the world less predictable.

Every day, our committed employees are there to serve our policyholders with personal care and attention. We tailor our services to what people really need by listening to what they have to say.

In 2025, we developed a new strategic plan that sets the course for the next five years. We stay true to our core: funeral insurance with care, quality, and commitment. That is where we want to excel and to make a difference for our customers. The new strategy gives us a three-pronged approach. We will continuously strengthen our services to improve the well-being of customers. We will accelerate innovation through digitalisation, among other things, so that our services better meet the needs of today and tomorrow. And we are taking extra steps to support customers in their well-being in the period before, during, and after a loved one dies. This course will lead to added value for customers, an organisation where employees are proud to work, and sustainable business continuity.

Stakeholders

DELA Natura maintains a structural dialogue with its stakeholders, including customers, employees, and suppliers. A standard part of our governance, this dialogue supports the quality of decision-making and strategic management.

In 2025, our stakeholder dialogue was further intensified to make more targeted use of the outcomes in defining and implementing our strategic course. We drew a distinction in that respect between a dialogue about material topics that are strategically relevant and the regular dialogue via departments and employees. This way of working was developed after consultation within DELA and with external experts; it included defining the protocols for providing the stakeholder groups with feedback.

We will use information from the regular conversations with our stakeholders and the more in-depth discussions about the strategically relevant topics as input for the successful implementation of our strategic course for 2026-2030. We take account of what is important to stakeholders, the environment, and our organisation. By truly engaging in dialogue and gaining insight into our choices, we will succeed in building on long-term relationships and a resilient organisation.

A structure aimed at collaboration

A structure aimed at collaboration

To achieve our strategic goals, we will require digital support, which is one area in particular where we see opportunities for organising across country borders. We have set up a management organisation to coordinate the creation of a strategic project portfolio, to professionalise and standardise our way of working, and to achieve synergy in our IT landscape. For this purpose, the three country IT organisations have been combined.

We aim to implement this plan based on three core principles:

- Ultimate customer focus – a clear, recognisable experience, accessible, personal, and tailored to customer needs

- Simplification – simple, replicable processes

- Disciplined execution – clear targets, clear roles, and continuous improvement

IT programmes

Digital Transition of the Insurance Chain

The Dutch long-range programme 'Digital Transition of Insurance' aims to replace the record-keeping systems for our insurance portfolio. The year 2025 was dominated by the migration of most of the DELA LeefdoorPlan policies from the old system to the new environment. This now also enables customers to make their own changes.

In Belgium, we will eventually transition to a new insurance record-keeping system as well. A preliminary study was completed for this purpose in 2025, and the main objectives were determined: to accelerate the launch of new products, make processes more efficient and reliable, and to retain local scope for taking action within the international organisation. Based on the study, it was found preferable for Belgium to use the same technology as in the Netherlands. We expect to increase the synergy and collaboration between the countries and to create room for further growth and development as a result of this transition.

In 2025, we continued our hard work to lay the technical basis for the Nalatenschapzorgplan (estate planning), our new Belgian insurance product that will be introduced in 2026.

DORA

The Digital Operational Resilience Act (DORA) entered force in 2025. The aim of this European law is to strengthen the operational resilience of financial institutions. Given our role in providing financial services, this also applies to DELA.

In 2025, we revised the programme for the remaining implementation process regarding governance, joint principles, and improved reporting structures across the countries. Because of the size and complexity of the law, several activities will continue into 2026. The emphasis lies on implementation in daily practice: demonstrating that the actions taken are effective.

Digital Finance

Digital Finance is a group-wide programme aimed at replacing outdated financial accounting software and providing the Belgian and Dutch entities with a modern and future-proof system. Various interfaces for communication with other systems have also been and continue to be updated.

In 2025, the real estate entity was connected up for Belgium. The plans for 2026 include connecting the insurance businesses in the Netherlands and Belgium.

Digital DELA customer contact accessible to all

With the requirements of the new European Accessibility Act to hand, DELA in 2025 took a great step forward in making digital products and services accessible to people with an impairment. Digital means of communication such as DELA's web pages and letters available in digital environments have been improved to make them easier to read (or to understand via audio) and navigate.

Data platform

In all countries, we have been focusing more and more on data as it forms the basis for better services and faster decision-making. We strengthen our data approach by centralising data, improving standards and governance, and making data more accessible within the organisation. That enables us to develop new products faster, design smarter processes, and optimise our supply of information.

Growth through strong relationships

Growth through strong relationships

We aim to grow by establishing strong relationships. That is reflected not only by our level of customer satisfaction and our reputation but also by the upward trend in the number of people that we insure.

Number of persons insured

Modest growth was achieved in the overall number of persons insured during 2025.

| 2025 | Net growth | 2024 | |

|---|---|---|---|

| Uitvaartplan (prepaid funeral insurance) | 3,087,003 | +20,295 | 3,066,708 |

| LeefdoorPlan (life insurance) | 267,507 | -7,284 | 274,791 |

| Spaarplan (savings-linked insurance) | 45,669 | -2,636 | 48,305 |

| Yarden (closed book) | 861,717 | -25,629 | 887,346 |

| Total Netherlands | 4,261,896 | -15,254 | 4,277,150 |

| - | |||

| Uitvaartzorgplan (funeral insurance) | 741,240 | +33,411 | 707,829 |

| Other (closed book) | 262,056 | -7,656 | 269,712 |

| Total Belgium | 1,003,296 | +25,755 | 977,541 |

| - | |||

| Aktiv Leben (life insurance) | 125,678 | +10,140 | 115,538 |

| Sorgenfrei Leben (prepaid funeral insurance) | 97,183 | +13,080 | 84,103 |

| Other (closed book) | 118,341 | -3,569 | 121,910 |

| Total Germany | 341,202 | +19,651 | 321,551 |

| Total | 5,606,394 | +30,152 | 5,576,242 |

We have seen a decrease in the Netherlands. The DELA UitvaartPlan portfolio grew, but the Yarden portfolio shrank now that it is no longer sold to new customers and because some of its current policyholders have died. In 2025, DELA's focus for the DELA LeefdoorPlan was on the migration of the portfolio to the new online platform. In the competitive market for term life insurance, this resulted in a relatively limited commercial drive during this period. Due to the debate on box 3 tax, there was also less demand for our savings-linked product.

We have offered customers an 'all set' check ('Goed Geregeld Check') so they can re-evaluate their needs and arrangements at their convenience. This quick check tells them whether their insurance and funeral arrangements are all set for the future. In 2025, all Yarden package policyholders were again informed about the arrangements made for their policy during the acquisition of Yarden in 2021.

The distribution strategy in Belgium has been paying off, and we are seeing encouraging growth. In 2025, we passed the one million mark for the number of people we insure in Belgium: a milestone that we are proud of. Great emphasis was also placed on the development of our new insurance product: the Nalatenschapzorgplan. This product provides estate planning and financial certainty for families so they can get on with their lives with peace of mind. This product will be introduced in 2026.

In spite of the less favourable economic situation in Germany, we have seen slight growth there as well. At the same time, however, competition is on the rise. Based on this growth perspective, we will further strengthen our distribution in controlled steps.

Customer satisfaction and reputation

Offering high-quality services is where it all begins. We measure the satisfaction of our customers at different points in time. This measurement forms the main input for management, learning, and improvement in this area. We use the Net Promoter Score (NPS) to measure customer satisfaction. The NPS (a widely used metric that reflects how likely customers are to recommend our products and services to others) shows a slight increase in customer satisfaction in the past year; and we are proud of that.

Net Promoter Score

| 2025 | Difference | 2024 | |

|---|---|---|---|

| Netherlands | 43 | -3 | 46 |

| Belgium | 65 | +4 | 61 |

| Germany | 57 | +8 | 49 |

| Group | 55 | +1 | 54 |

In the Netherlands, we have seen a slight decrease in customer satisfaction in spite of the targeted action to optimise our website, our communication with customers, and MijnDELA. The way in which questions are handled could stand further optimisation in particular. Customer satisfaction in Belgium saw a further increase, which was due in part to online customer journeys and a proactive approach to customers.

We made improvements in areas such as the user-friendliness of online platforms, streamlined customer inflow, and ensured clear information and support for premium payments and customer interaction. These initiatives contributed to heightened efficiency in the provision of our services and a better customer experience. In the German market, insurance intermediaries traditionally play an important role in addition to the online channel. We are proud that, with an NPS of 57, we enjoy the highest level of customer satisfaction in the German market for funeral and life insurance.

In Belgium, we received the DECAVI award in October 2025 for the ninth time in a row for the best funeral insurance in the Belgian market. DECAVI is an independent external organisation that annually presents awards for both life and non-life insurance products.

In the German market, insurance intermediaries traditionally play an important role in addition to the online channel. We are proud that in 2025 we still have the best funeral insurance (without a waiting period) (2025 Beste Risikolebensversicherungen according to WirtschaftsWoche) and term life insurance in the German market (2025 Risikolebensversicherung 'sehr gut' according to Handelsblatt).

Reputation score (StakeholderWatch pulse)

| 2025 | Difference | 2024 | |

|---|---|---|---|

| Netherlands | |||

| Members | 81 | - | 81 |

| Non-members | 67 | - | 67 |

| Total | 74 | - | 74 |

| Belgium | 71 | +4 | 67 |

| Group | 73 | +2 | 71 |

DELA enjoyed a robust and strong reputation in the past calendar year. In comparison with the previous year, we saw a slight increase of two points, which shows that our activities aimed at maintaining and strengthening our reputation are paying off. The Dutch and Belgian brand campaigns definitely helped to build our strong reputation. Both policyholders and non-policyholders in the Netherlands perceive DELA as reliable, successful, and socially responsible. In Belgium, we saw our reputation rise once again. In 2025, we strengthened our name in the Belgian market.

We do not yet specifically measure our reputation in Germany. Our focus here is on building up our core activity and infrastructure. We will measure our reputation and monitor the results as we continue to grow. A brand campaign for Germany has been prepared for 2026.

Employees

Our employees are crucial to serving our policyholders. Engagement, integrity, and business sense are at the heart of everything we do. As part of our good employment practices, we invest in our employees to ensure they are engaged, proud, and healthy and have room for personal development. DELA Natura had 775 employees (682 FTEs) at year-end, the majority of whom are based in the Netherlands.

Employee satisfaction

We see the results of the employee experience survey among the permanent employees in the Netherlands, Belgium, and Germany as a key indicator of how the well-being of our employees is developing. This involves assessing the employee Net Promoter Score (eNPS) and asking all sorts of questions about good employment practices, engagement, social safety and inclusion, leadership, teamwork, ownership, customer centricity, and change management.

Employee Net Promoter Score

| 2025 | Difference | 2024 | |

|---|---|---|---|

| Netherlands | 30 | -14 | 44 |

| Belgium | 54 | - | 54 |

| Germany | 10 | - | 10 |

| Total | 31 | -12 | 43 |

At 31 points, Natura's eNPS remains high. However, this is lower than last year, mainly due to a decrease in employee satisfaction in the Netherlands. This development is connected to points for improvement around the timely supply of information, the design of our working processes, and capitalising on ideas and suggestions from employees. That serves as a basis for targeting improved communications, process optimisation, and taking action on feedback, with teams and departments also addressing their own results. In Belgium and Germany, employee satisfaction remained the same as in the previous year.

Thanks to the high scores for good employment practices in the employee experience survey, DELA in the Netherlands and Belgium received Effectory's World-class Workplace label. This label is for organisations that outperform the benchmark for eNPS and employment practices.

Absenteeism

It is important to us for all employees to be physically and mentally healthy and able to perform their job, both now and in the future. The employee experience surveys show to what extent employees experience a good work-life balance and how they experience the pressure of work. We also monitor absenteeism monthly by department, location, and region to evaluate whether existing actions are effective and additional actions are needed. Additional actions are taken at team, location, department, country, or even group level if the results of the employee experience survey, the absence rate, or an unfavourable employee turnover rate so dictate.

The absenteeism rate for DELA Natura's employees in 2025 due to sickness, personal reasons, and other causes was 4.7 per cent in the Netherlands (2024: 4.0 per cent), 8.2 per cent in Belgium (2024: 6.6 per cent), and 7.2 per cent in Germany (2024: 6.5 per cent). Absence due to sickness rose in all the countries in comparison with the previous year in spite of our efforts in the area of health, safety, and prevention. It is important to us for all employees to be physically and mentally healthy and able to perform their job, both now and in the future. That is why we invest in a range of initiatives, such as training on how to deal with inappropriate behaviour and first aid, as well as sickness prevention programmes and the personal responsibility model.

Sustainability

As a public-interest entity, DELA Natura recognises its responsibility to contribute to a sustainable future. DELA Natura complies with the Dutch Non-Financial Reporting Decree/European Non-Financial Reporting Directive (NFRD) by publishing material sustainability-related information on, for instance, the environment, employees, and diversity in governance in the sustainability report of DELA Coöperatie U.A., Eindhoven (jaarverslag2025.dela.nl).

DELA Natura is also required to comply with the EU taxonomy. This is a classification system that identifies economic activities that can be considered environmentally sustainable. This helps companies and investors determine which activities substantially contribute to various environmental objectives without significantly harming other environmental objectives. The result is enhanced transparency and comparability of sustainability-related information.

DELA Natura reports in accordance with Delegated Act 2026/73. Within the framework of the EU taxonomy, we consider the predominant nature of DELA Natura to be that of an insurer. Insurers and other financial institutions may choose not to publish any comprehensive reports as they await further developments in the EU taxonomy. DELA Natura exercises this option and affirms that no activity is claimed as being associated with economic activities that qualify as environmentally sustainable pursuant to Articles 3 and 9 of Regulation (EU) 2020/852 (taxonomy regulation).

Affordable and scalable

Affordable and scalable

Our policyholders should be able to look to the future with as much confidence as possible with inflation-proof funeral insurance that we offer for the lowest possible premium. We aim for an optimum balance between equity, profit sharing, and solvency.

Operating profit (loss)

Operating profit (loss) is the profit or loss generated from our core activities. This is the profit or loss before the investment return (excluding the part that is allocated to the operating profit or loss), exceptional income and expenses, profit sharing, and taxes.

| Amounts x €1,000 | 2025 | Difference | 2024 |

|---|---|---|---|

| Premium income | 774,505 | 30,563 | 743,941 |

| Investment income allocated to operating profit (loss) | 220,581 | 15,622 | 204,959 |

| Underwriting expenses | -705,816 | -23,622 | -682,194 |

| Technical margin | 289,270 | 22,563 | 266,706 |

| - | |||

| Operating expenses | -175,717 | -9,896 | -165,821 |

| Acquisition costs (excluding allocated acquisition costs) | -22,675 | -2,428 | -20,247 |

| Operating profit (loss) | 90,878 | 10,239 | 80,638 |

The €90.9 million in operating profit from insurance business was a €10.2 million increase on 2024. This was mainly attributable to the steady growth in the portfolio and the increase in premiums rates.

Investment result

The net return on investment for 2025 was a 5.7 per cent gain (2024: 6.8 per cent gain). The return on shares was 15.8 per cent, and 3.4 per cent on fixed-income securities. Real estate investments yielded a return of 1.0 per cent. The return on infrastructure investments was 3.3 per cent, with agriculture and forestry investments yielding 1.4 per cent.

The value of our investment portfolio fluctuates due to trends in the financial markets. We invest with a specific goal: to achieve a sufficient return to guarantee a dignified funeral for the lowest possible premium in the future as well. The nature of our insurance policies (which are in most cases paid out upon death) translates into long-term obligations. By accepting a calculated risk in our investment strategy, we are able to achieve the required results over the years. Fluctuations in the value of our investment portfolio are a consequence of this policy.

Development of technical provisions

The technical provisions, including a provision for profit sharing and minus deferred acquisition costs and reinsurance, increased by €563.8 million. The technical provisions in our balance sheet are based on fixed principles, such as an actuarial interest rate. The impact of higher or lower market interest rates and/or inflation is therefore not reflected in this balance sheet item. Measured in market value (Solvency II), the technical provisions decreased by €210.5 million. Because of these developments, the surplus on the technical provisions has increased, as shown by the adequacy test.

Coverage ratio

The coverage ratio represents the market value of investments as a percentage of the market value of guaranteed liabilities and is influenced by factors such as interest rates, mortality, and costs. The coverage ratio at the beginning of the reporting year was 200 per cent, ending in 2025 at 241 per cent. Because of the higher interest rates and adapting to the Solvency II calculation rules, the coverage ratio increased by 30 percentage points. Developments in the insurance portfolios pushed the coverage ratio up by four percentage points. Investment income resulted in a seven percentage point increase.

Coverage developments in percentage points:

| Start of year | Tightening effect |

Relaxing effect |

Year-end | |

|---|---|---|---|---|

| Start of year | 200% | |||

| Other factors | 0% | |||

| 0% | ||||

| Increase in interest rates and adaptation to Solvency II calculation rules | 30% | |||

| Developments in insurance portfolio | 4% | |||

| Investment result | 7% | |||

| 41% | ||||

| Year-end | 241% |

Profit share

The balance between healthy solvency, sufficient equity levels, and profit sharing is important for the financial health of our organisation. In 2025, a profit share of €264.8 million was awarded (2024: €281.2 million). The inflation on funeral costs was 5.00 per cent (2024: 5.84 per cent). Thanks in part to the high average coverage ratio, this year we were able to award a 100 per cent share of the profit to policyholders of DELA UitvaartPlan in the Netherlands and 87 per cent to policyholders of the funeral product in Belgium.

| Amounts x €1,000 | 2025 | 2024 | 2023 | 2022 |

|---|---|---|---|---|

| Awarded | 264,798 | 281,247 | 249,224 | 43,654 |

Premium adjustment

About 55 per cent of policyholders have the Dutch DELA UitvaartPlan (DUP). As at 1 January 2026, the premium for this insurance has increased by 5.00 per cent (last year at 1 January 2025: 5.84 per cent). This is the same as the expected inflation on the funeral costs at 1 January 2026.

If the cost of a funeral rises due to inflation, more premium must also be paid over the previous years. We call this extra premium over past periods the past-service costs. This year, however, those did not lead to an increase of premium, as we were able to fund all of the past-service costs from the annual profit share. Nor has there been any additional increase in premium rates, known as 'premium action'. The total increase of premium at 1 January 2026 therefore remains the same as the inflation on funeral costs.

Solvency ratio

DELA determines its solvency on the basis of Solvency II, hence the name Solvency II ratio. This European calculation framework takes into account the risks recognised in the balance sheet of the insurer when determining solvency.

The solvency ratio increased from 201 per cent to 213 per cent at year-end and remains robust.

The Solvency II ratio decreased by eleven percentage points on the back of developments in investment income, equity markets, interests rates, and inflation. Developments in the insurance portfolio during 2025 reduced the ratio by three percentage points. Changes to the underwriting parameters resulted in a three percentage point increase. Effective 2025, all insurance activities are taxed in the Netherlands, regardless of whether the policies are managed at our head office in the Netherlands or at one of our branches in Germany or Belgium. That has a positive impact on the mitigating effect of taxation, with the Solvency II ratio increasing by seven percentage points. Other changes to models, such as adapting the coverage ratio to the Solvency II calculation rules, resulted in a 16 percentage point increase.

Solvency ratio developments in percentage points:

| Start of year | Tightening effect |

Relaxing effect |

Year-end | |

|---|---|---|---|---|

| Start of year | 201% | |||

| Change to economic parameters (interest, inflation, volatility), asset mix, and investment results | -11% | |||

| Developments in insurance portfolio | -3% | |||

| -14% | ||||

| Change to underwriting parameters | 3% | |||

| Other factors | 23% | |||

| 26% | ||||

| Year-end | 213% |

Strong and clear governance

Strong and clear governance

Corporate governance at DELA stands for prudent management, good oversight, and transparent accountability. We comply with national laws and regulations, European directives and regulations (including Solvency II), and policy rules. As a voluntary member of the Dutch Association of Insurers, we commit to complying with several standards, such as the Dutch Code of Conduct for Insurers. Compliance with these codes of conduct by the members of the Dutch Association of Insurers is monitored by the foundation for insurer compliance, Stichting toetsing verzekeraars.

The design of our governance structure is set out in a governance charter, which we regularly evaluate and update where necessary.

Legal structure, licences, and supervision

DELA Coöperatie U.A. (also referred to in this report as 'DELA', 'DELA Group' or 'Coöperatie DELA') is a cooperative with excluded liability for its members.

DELA Coöperatie U.A. holds all the shares in DELA Holding N.V.

DELA Holding N.V. includes three principal companies: DELA Natura- en levensverzekeringen N.V. (hereinafter: DELA Natura), DELA Uitvaartverzorging N.V., and DELA Holding Belgium N.V.

DELA Natura accommodates all Dutch, Belgian, and German insurance activities. The Belgian and German insurance activities are conducted via a branch of the Dutch insurer in those countries.

As an insurer, DELA Natura, including its branches in Belgium and Germany, is subject to the prudential supervision of the Dutch central bank (DNB). In addition, DELA Natura is subject to the supervision of the Authority for the Financial Markets (AFM) in the Netherlands, the Financial Services and Markets Authority (FSMA) in Belgium and the Federal Financial Supervisory Authority (BaFin) in Germany as concerns business conduct supervision for insurance activities.

DELA Uitvaartverzorging N.V. is responsible for the funeral activities in the Netherlands. Belgian funeral activities fall under DELA Holding Belgium N.V.

Supervision and governance

At DELA Natura, supervision and governance are divided between the Supervisory Board and the Management Board.

Supervisory Board

The Supervisory Board is the supervisory body of DELA Coöperatie U.A., DELA Holding N.V., and DELA Natura- en levensverzekeringen N.V. Members of the Supervisory Board are appointed by the general meeting on the recommendation of the Supervisory Board. The Supervisory Board consists of at least five and no more than seven members, if possible with two representatives of the general meeting of DELA Coöperatie U.A.

The Supervisory Board oversees the Management Board and advises it about objectives, strategy, risks, and laws and regulations. The Supervisory Board approves, among other things, the financial statements, budget, large investments, and the remuneration policy, nominates members of the Executive Board, and assesses the performance of the Management Board. The Supervisory Board acts in the interest of the company, carefully balances the interests of stakeholders, and works according to internal rules. In principle, members of the Supervisory Board are appointed for a term of four years. They may be reappointed for a second terms of four years and for another two terms of two years each up to a total of twelve years.

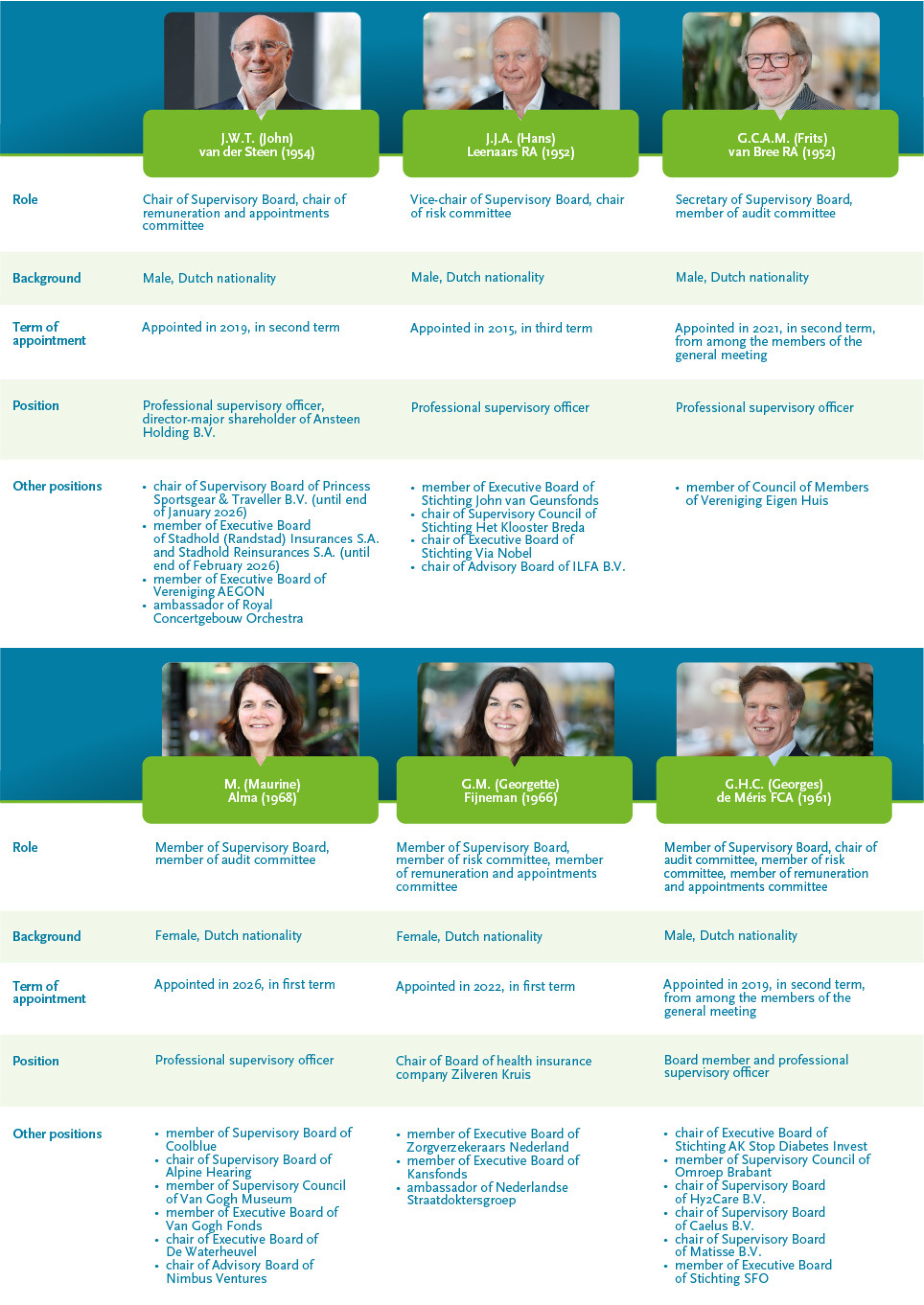

For the proper performance of its tasks, the Supervisory Board has established an audit committee, risk committee, and a remuneration and appointments committee. These committees prepare decision-making by the Supervisory Board and advise the Supervisory Board and the Management Board. The composition of the Supervisory Board and its committees is illustrated below.

On 31 January 2026, Mrs Caderius van Veen stepped down from the Supervisory Board as her final term ended after 12 years. On that same date, Mrs Alma was appointed as a member of the Supervisory Board for a first term of four years.

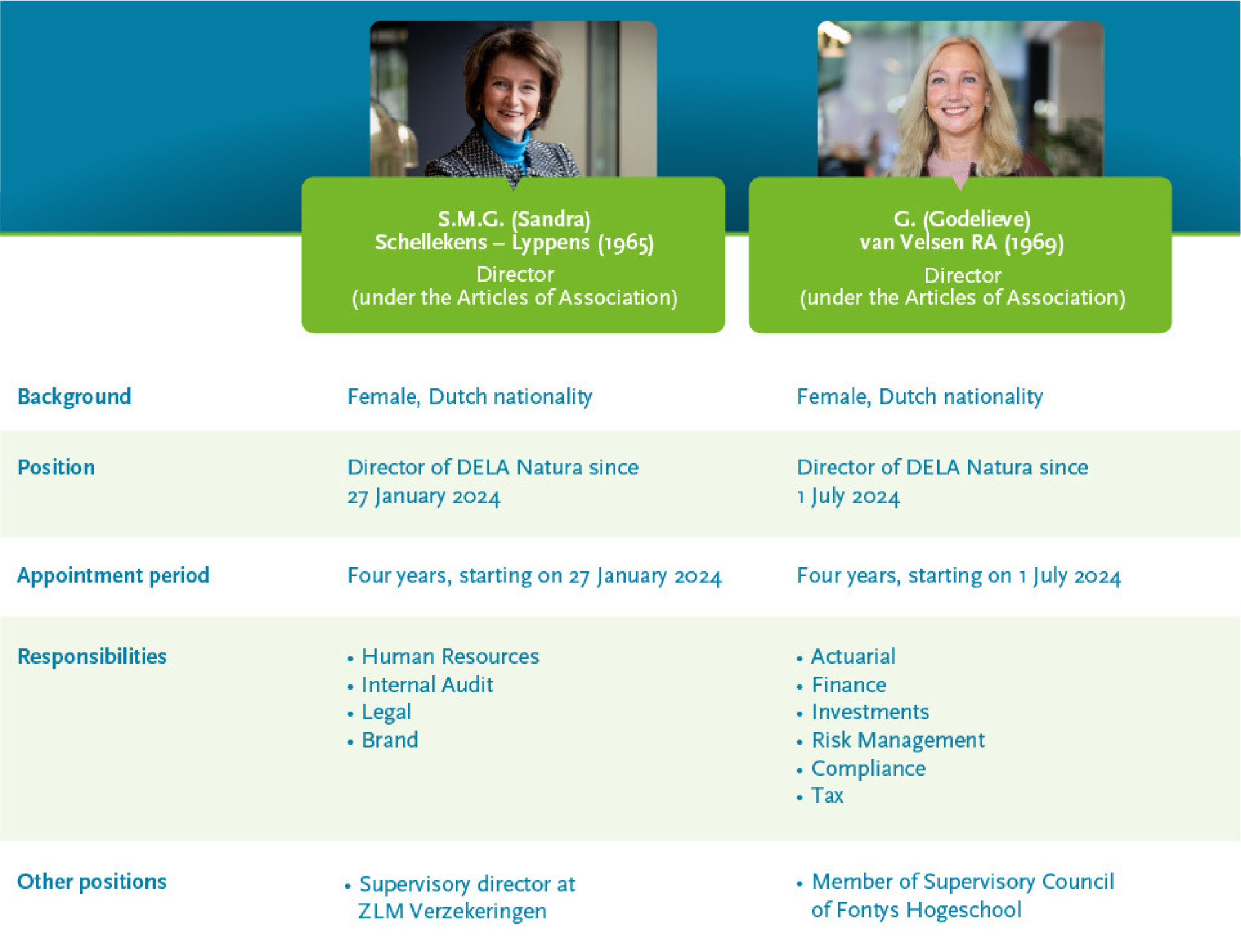

Management Board

DELA Natura has a Management Board consisting of a number of natural persons determined by the Supervisory Board. In 2025, the Management Board consisted of two female directors. The Management Board is, except for the restrictions in the Articles of Association, responsible for directing the company and managing its assets. The Management Board may decide which task is entrusted to each director in particular. This division of tasks must be approved by the Supervisory Board.

Investment advice committee

The Asset Management department carries out the investing activities for DELA Natura. DELA has an investment advice committee that advises the Management Board and the Supervisory Board about investments regarding policy recommendations, policy changes, and carrying out the investment policy.

The investment advisory committee evaluates whether proposals are consistent, comprehensive, and sound with regard to return, risk, and sustainability. The investment advice committee consists of at least three external persons. The Supervisory Board appoints the members of the investment advice committee on the recommendation of the Management Board.

Risk management

As DELA Natura, we manage risks to achieve our long-term goals, protect the interests of our stakeholders, and safeguard our company's future. By identifying and managing risks at an early stage, we remain financial healthy, organisationally flexible, and trusted in society.

Organisation

Our risk management provides insight into strategic, financial, operational, and integrity risks. The aim is clear: to base our management on and anticipate changing situations and back up responsible choices with reliable information.

DELA applies the Three Lines Model for risk management and control.

We safeguard the independence of the second and third lines so that the risk management system can function effectively.

Process

Our risk management process provides constant insight into the main risks. This process also ensures that we carefully weigh up our internal controls. The CFRO is responsible for this process.

Identifying risks

We classify risks into four main categories:

- Strategic risks – choices and changes in policy, market, or organisation

- Financial risks – fluctuations in financial markets and insurance trends

- Operational risks – errors, operational risks, incidents or the failure of processes

- Integrity risks – non-compliance with laws and regulations

Please refer to the financial statements for more detailed information about the risks per risk category. See 'Financial statements', 'Notes to the balance sheet and income statement', '3. Risk section'.

Defining risk appetite and limits

Our risk appetite is the amount of risk that we are willing to accept in order to achieve an optimal balance between risk, return, and resilience. That balance is vital for achieving our goals and generating value for members and policyholders.

Our risk appetite per risk category is as follows:

- Strategic risks – neutral risk appetite based on solidarity and our core values, with a view to interests and prospects for stakeholders and valuable products and services for our members

- Financial risks – neutral risk appetite aimed at robust solvency and long-term value creation for our policyholders through a well-spread investment portfolio and managing financial risks

- Operational risks – neutral risk appetite aimed at managing operational risks

- Integrity risks – low risk appetite aimed at compliance with laws and regulations

In addition to our risk appetite, we work with specific risk appetite statements that include key risk indicators (KRIs) with associated risk limits and tolerances. Our KRIs show when risks increase or tighter control is required.

Risk management

Strategic risks

The aim of the strategic risks that we take is to find a good balance between growth, efficient business operations, and business continuity. Every year, we formulate specific annual targets for achieving our strategic objectives. Progress on these annual targets is monitored on a monthly basis, with the necessary adjustments.

Financial risks

The aim of taking financial risks is to achieve an optimal balance between healthy solvency, sufficient equity levels, and controllable premium increases for our policyholders. For funeral insurance, we seek to guarantee an affordable and dignified funeral for our policyholders. Therefore, we accept investment risks in this sense to achieve a return that we can preferably share with our policyholders through profit sharing to cover the service costs associated with the rising cost of funerals due to inflation. To monitor these risks and returns, we have a system of risk appetite statements that is aimed at guaranteeing the desired optimal balance.

Operational and integrity risks

The aim of controlling operational and integrity risks is to have controlled business operations and to comply with laws and regulations. We have defined the main risks and established internal controls for them, which are regularly assessed. We have a system of operational risk appetite statements in place to monitor the risks. These statements act as an early warning system. If a limit is exceeded, it can be a sign that risks are not adequately controlled and that remedial action is required or that the internal controls need to be tightened up.

Mitigating actions

Risk mitigation actions are taken to ensure the risks remain within the desired bandwidths. In most situations we use a mix of:

- terminating or outsourcing activities;

- reducing risks by taking preventative action or by increasing our internal controls;

- transferring risks via insurance/reinsurance and/or contract management;

- accepting risks that can be borne by the organisation itself.

We take extra measures if the risks exceed the limits and/or are larger than desired. Limits may only be deliberately exceeded – temporarily – if approved by the Management Board.

Monitoring and reporting

We test the effectiveness of the internal controls every six months. That gives us a picture of our net risk positions, so we can assess whether the risks remain within the limits of our risk appetite. Every six months as well, we test whether the risk limits and tolerances (KRIs) have been exceeded.

The basic idea is to reduce risks that exceed our risk appetite to a lower risk level by using a mix of risk mitigation solutions. Additional actions are defined if limits are exceeded. If a KRI limit is exceeded, it is a sign that a risk has manifested itself. That can be a reason to take remedial action or to tighten up the internal controls.

Management regularly goes through the Risk Control Self Assessment (RCSA) process. That results in an 'in control statement' (ICS). In addition, the Internal Audit department evaluates the design and effectiveness of the risk management system.

Own risk and solvency assessment

As part of Solvency II, we achieve a proper balance between risk, capital, and strategy. The own risk and solvency assessment (ORSA) covers that process. This involves reviewing our company objectives, risk appetite, and available capital buffers in relation to various scenarios (stress scenarios). These scenarios are defined by the Management Board prior to the ORSA, with advice from the second line. We record the findings in an ORSA report.

Findings in the ORSA

- Our solvency is robust.

- The coverage ratio in the basic scenario shows a gradual increase.

- Adjustment is necessary in environments with low interest rates and low inflation.

- Climate stress scenarios show that the sensitivity of our financial position to physical and transition risks is limited.

In short: our capital and our risk structure are solid, with an emphasis on future vulnerabilities.

Capital management

Our capital policy is aimed at maintaining a sound solvency position. We constantly strive for a good balance between the amount of capital we maintain and the risks we face. We have developed an internal minimum solvency capital requirement. In this framework, we have defined an internal minimum solvency capital requirement which we always aim to exceed. The internal minimum solvency capital requirement for DELA Natura has been established at 150 per cent.

The capital policy defines various actions should the solvency ratio drop below the internal minimum solvency capital requirement. The solvency ratio was constantly higher than the solvency requirement during 2025.

Developments in 2025

In 2025, we evaluated the risk appetite statements and optimised them where necessary. In this section, we discuss the risks faced in 2025 and the measures we took to limit their probability and/or impact. We also look at the general measures that we took to reduce risks.

Strategic risks

Strategic risks can obstruct us in achieving our long-term goals. Regular review of our strategy contributes to the reduction of strategic risks. In 2025, we worked on a new long-term business plan for 2026-2030, which will be implemented in tandem with organisational transformation. Starting in 2026, we will organise ourselves primarily in business units for our insurance activities and our funeral activities.

Financial continuity is essential for implementing our strategy. Stress tests show that while our solvency position is robust, our equity position is sensitive to scenarios with low interest rates and low inflation. We take preparatory measures or make different choices where necessary. The main preconditions and actions are set out in our capital policy, which is evaluated annually. We do not maintain any required capital for strategic risks.

Financial risks

We monitor developments in the financial markets on an ongoing basis. In 2025, this resulted in extra currency hedging for our exposures to US dollars.

More detailed information on the development of the financial risks (including the associated quantification) is provided in the risk section of the financial statements.

Operational risks

Operational risks are caused by external influences, human error, and the failure of processes and systems. Despite clear processes, responsibilities, and reporting, we cannot completely eliminate these risks. The number of incidents in operational risk management are limited. It is important to learn from the past to prevent repeats in the future. The nature and scope of these incidents is very diverse, varying from fraud (or attempted fraud) and cyberattacks to operational incidents. We have assessed these incidents, and we have taken additional measures where necessary.

In 2025, we continued the 'Business in Control' programme and integrated it into our regular business operations. In addition, 2025 saw completion of the centralised registration of risks and internal controls for the Dutch business; the internal controls will be regularly assessed. We also started on the centralised registration of risks and internal controls for the Belgian and German operations, where that is still performed locally.

Integrity risks

Non-compliance with laws and regulations is a risk that can threaten our continuity and tarnish our reputation. At the same time, the regulations that we must comply with continue to grow, such as the DORA requirements that took effect in 2025. There were no serious incidents related to integrity risks in 2025. To further control the risk, in 2025 we worked on our professionalisation for a variety of topics, such as sanctions legislation. An important part of that was compliance with the current laws and regulations on sanctions.

Ambitions for the future

Ambitions for the future

We are confident – and realistic – about the future. We continue to build on what we have achieved so far and make choices to remain relevant in the coming decades as well.

In 2026, we will take our first steps towards implementing our new strategic course as we pool our strengths across national borders more than ever before. We are working on an attractive and future-proof portfolio of insurance products. In Belgium, we are preparing to introduce a new insurance product that gives bereaved families financial peace of mind and support for their other concerns when someone dies.

Our employees play a central role in this endeavour. They form the heart of our organisation. We provide room for development, responsibility, and initiative so they can do their job with professionalism and commitment. In 2026, we developed a vision for the skills that we need for the future, both in leadership and within the organisation as a whole.

We are also investing in technology and process improvement so that we can adapt to changes more quickly and keep developing our services. We are working on a modular application landscape that supports flexibility and resilience.

In addition, sustainability remains an important part of our course. We are taking further steps to reduce our ecological footprint and are investing in employee vitality and long-term employability.

Finally, we are careful with our resources as we safeguard our financial basis. That helps us keep our services accessible while continuing to invest in quality, innovation, and the future of our organisation.

Our policyholders are at the heart of everything we do. It is through our continuous investment in people, processes, products, and services that we are able to promote their well-being. Our employees, suppliers, and partners make all the difference in that area every day, and we are very grateful to them for their hard work and commitment.

Eindhoven, 21 April 2026

The Management Board

Sandra Schellekens

Godelieve van Velsen