Business model

Business model

DELA Natura is the insurance provider within the DELA Group and focuses specifically on the development and expansion of insurance activities. With our strong collective purchasing power and the investment of contributions, we ensure funeral insurance policies hold their value and that premiums remain affordable — even for policies that will only be paid out many decades from now.

Our business model provides a solid foundation that supports us in achieving our ambition.

Ambition

"We provide financial security and relieve our members and customers of concerns related to 'passing on and remembrance’."

It is important to continue growing in order to achieve this ambition. We do so by offering and expanding our range of products and services, anticipating the current and future needs of customers.

Stakeholders

DELA Natura collaborates with a wide range of organisations, customers and other parties on a daily basis. These groups collectively form our network of stakeholders. Actively engaging in dialogue with them strengthens relationships and fosters mutual understanding and trust. This ongoing exchange enables us to gain valuable insights which help us optimise our core activities and respond more effectively to the needs and expectations of stakeholders. By taking their feedback and suggestions seriously, we contribute to a sustainable and transparent way of doing business. And this ultimately leads to shared value creation.

Our main stakeholders are shown in the image below.

Stakeholder dialogues are an integral part of our approach, encompassing customer service interactions and periodic evaluations with partners and suppliers. Formal meetings, such as those with regulators form part of our stakeholder dialogue. Our relationship with policyholders extends beyond insurance policies alone as we foster long-term connections. We use direct communication methods.

In the coming year we will formulate a new multi-year strategy for 2026-2030. This will incorporate customer feedback highlighting the need for further innovation of our core activities in insurance. This process will enable us to continuously improve our services and develop new ones that promote solidarity.

Working together is another key priority for us as we actively engage with industry organisations. This includes the insurance sector (Verbond van Verzekeraars and Assuralia). Working together also facilitates the sharing of knowledge and experiences, ultimately enhancing the quality of our services.

Developments

A number of developments can potentially influence the successful realisation of our ambitions, making it vital to monitor and, where possible, anticipate them. The following six trends had a significant impact on our operations in 2024:

1. Financial turbulence

The year 2024 saw a mixed financial landscape. Despite the geopolitical unrest, 2024 was a strong year for financial markets. The average inflation in the Netherlands reached 3.3%(source: Statistics Netherlands), which is a significantly lower figure than in earlier years but higher than the rest of the Eurozone. This inflation was primarily driven by increased demand, rising rents and higher wage growth.

Despite the financial turbulence, our strong coverage ratio enabled us to provide a record profit-sharing amount of over €281.2 million. The premium for the DELA Uitvaartplan policy in the Netherlands rose by 5.84% on 1 January 2025. Without the profit-sharing scheme, the increase would have been 10.28%.

2. Growing competition: customer satisfaction, local presence and distinctive strength remain key

The Dutch insurance sector is going through a strong consolidation process. The Belgian insurance market is significantly more fragmented than in the Netherlands and Germany, with the latter essentially having only three major players.

Therefore, we are expanding our range of products and services. DELA Natura continues to work hard to maintain and enhance customer satisfaction, with various quality programmes in place to ensure everyone experiences the same high level of care and attention.

3. Increased sustainability

Sustainability is becoming an increasingly important theme. Our related strategy focuses on two key areas: reducing CO₂ emissions and lowering the energy consumption of our locations. DELA is committed to the goals of the Paris Agreement, aiming to reduce our greenhouse gas emissions to net zero by 2050. The implementation of this strategy for our own operations is secured through the climate transition plan, which was first drawn up in 2024. The climate transition plan clearly outlines what is needed to successfully reduce our CO₂ emissions in line with the Paris Agreement. The socially responsible investment policy outlines what this means for our investments.

4. Pressure on the labour market

Labour market pressure remained a challenge in 2024. The Netherlands, Belgium and Germany currently have the tightest labour markets in Europe, resulting in higher recruitment costs for us. We aim to reduce workload and offer attractive employment conditions. We provide flexibility in working conditions and address factors such as employee well-being, absenteeism, onboarding processes and opportunities for career progression and development. Concrete examples of our efforts include a sabbatical scheme, a training programme for future managers and a personal vitality budget for each employee.

5. Diversity

Diversity and inclusion are also key priorities for DELA Natura as an employer. As DELA Natura we are committed to ensuring our workforce reflects the society we serve, that everyone has equal opportunities, and that employees feel safe to be themselves. We are currently developing a plan to promote diversity, equality and inclusion, which is set to be finalised in 2025.

6. Digitisation

The process of digitisation at DELA focused in 2024 on enhancing our services and increasing customer satisfaction. As a group, we are investing in a user-friendly online portal for taking out policies and simplifying administrative processes. In addition to offering opportunities, digitisation also poses risks. A good example is in the area of privacy. Digital threats such as phishing, ransomware, third-party attacks and more represent risks that we must address. Our commitment to privacy protection is not only a legal requirement but also a fundamental value for fostering good relationships with our policyholders. We understand that our customers' trust depends, among other things, on the careful and secure handling of their personal information.

7. (New) legislation and regulations

The focus on stricter regulations – particularly in the areas of transparency, risk management, sustainability and corporate governance – continued to increase. Businesses must comply with new national and international regulations, such as CSRD, DORA, GDPR and sanctions legislation. DELA Natura devoted significant attention to these regulations in 2024 and we expect this focus to remain a priority in the coming years. The fact that more regulations are being shaped at the European level requires an approach that extends across borders. To meet these requirements efficiently and effectively, we are increasingly seeing cross-border cooperation in the countries in which we operate. This also increases our efficiency and effectiveness. Additionally, we have a programme in the Netherlands called 'Business in Control' that is aimed at managing operational and compliance risks more effectively. We will continue with the implementation of this programme in 2025.

8. Changing personal preferences

At DELA Natura, we also observe shifting consumer behaviour across different generations. Whether it concerns baby boomers or Gen Z, each group has its own preferences. Financial circumstances also have an impact so we are increasingly focusing on customisation and a personalised approach. We are also increasing the accessibility for those looking to take out a funeral insurance policy (online). The introduction of a new CRM system for our Belgian customers and members will further enhance our ability to tailor our services and communications to individual preferences.

Results

Results

This section presents the results for the 2024 financial year and is divided into insurance, customer satisfaction and reputation, employees, operations, finance and sustainability.

Insurance

Modest growth was achieved in the overall number of policyholders during 2024. There was, however, a decline in the Netherlands as consumers increasingly factor price into their decisions. We also observed an increase in policy lapses, driven by factors such as excess mortality and cancellations, and particularly among those who took out insurance during the COVID-19 pandemic. The Yarden portfolio is being gradually phased out and no commercial activities are underway to add new policies. To address these changing customer needs, we are implementing a proactive marketing strategy, improving the online insurance application process, introducing new insurance products, and deploying a new CRM system. Ongoing discussions regarding Box 3 taxation continue to dampen demand for our savings product in the Netherlands.

In Belgium, our refined distribution strategy is paying off, and we are seeing significant growth. The number of reported Belgian policyholders has been adjusted. The implementation of a new data platform refined the definitions, leading to a more accurate and transparent representation of this figure.

We have also achieved significant growth in Germany despite the fact that a challenging economic situation affected consumer spending patterns in the country.

Number of policyholders per product at the end of the year and growth in reporting year

| 2024 | net growth | 2023 | |

|---|---|---|---|

| Uitvaartplan (funeral insurance) | 3,066,708 | +12,647 | 3,054,061 |

| Leefdoorplan (life insurance) | 274,791 | -5,970 | 280,761 |

| Spaarplan (savings insurance) | 48,305 | -4,852 | 53,157 |

| Yarden | 887,346 | -21,247 | 908,593 |

| Total Netherlands | 4,277,150 | -19,422 | 4,296,572 |

| - | |||

| Uitvaartzorgplan (funeral insurance)* | 707,829 | +37,160 | 670,669 |

| Inactive portfolios (closed book)* | 269,712 | -7,615 | 277,327 |

| Total Belgium | 977,541 | +29,545 | 947,996 |

| - | |||

| Aktiv leben (life insurance) | 115,538 | +12,172 | 103,366 |

| Sorgenfrei leben (funeral insurance) | 84,103 | +18,554 | 65,549 |

| Other portfolios (closed book) | 121,910 | -3,548 | 125,458 |

| Total Germany | 321,551 | +27,178 | 294,373 |

| - | |||

| Total | 5,576,242 | +37,301 | 5,538,941 |

Customer satisfaction and reputation

Being our primary stakeholders, we provide policyholders with financial security. Insurance is one of our core activities. We are active in the Dutch, Belgian and German markets with insurance products.

Providing high-quality services remained a top priority in 2024. Customer satisfaction levels with our personal services are measured at various times, and the results form the basis for guidance, learning and improvement in this area. Satisfaction levels are measured using the Net Promoter Score (NPS), a common indicator that reveals the extent to which customers would recommend products and services to others. The results show that customer satisfaction remained high, which we take great pride in.

| 2024 | difference | 2023 | |

|---|---|---|---|

| NPS | |||

| Netherlands | 46 | +3 | 43 |

| Belgium | 61 | +2 | 59 |

| Germany | 49 | -4 | 53 |

| Total | 54 | +1 | 53 |

Important positive feedback received from the customer satisfaction survey includes our fast and appropriate responses and the degree of personal attention. Customer services actively focus on directly resolving inquiries so that people are helped quickly and efficiently. Furthermore, we have made improvements by paying continuous attention to providing the right customer experience.

DELA Natura strives for maximum alignment with customer wishes and assesses this in the Netherlands using the 'Golden Ear' standard. The recognition aligns with the enhanced requirements in the area of customer focus and improvement management found in the ISO 9000 series.

In Belgium, we again received the DECAVI award in 2024 as the best funeral insurance on the Belgian market. DECAVI is an independent external organisation that annually presents awards for both life and non-life insurance products. In Germany, DELA was again recognised as Maklers Liebling (Brokers’ Favourite) in 2024, achieving first place with the Sterbegeld product and second place with Risikoleben.

While customer satisfaction in Germany remains high, we have observed a decline compared to last year. We are confident that addressing the underlying technical challenges will lead to a renewed upward trend in customer satisfaction.

DELA maintained a strong and robust reputation in 2024, and our activities are focused on preserving and further strengthening this. The reputation is measured for the DELA Group as a whole and the results are also defining for DELA Natura as we use the same brand name.

Reputation score (stakeholderwatch pulse)

| 2024 | difference | 2023 | |

|---|---|---|---|

| Netherlands | |||

| Members | 81 | +3 | 78 |

| Non-members | 67 | +1 | 66 |

| Total | 74 | +2 | 72 |

| Belgium | 67 | +4 | 63 |

| Total | 71 | +3 | 68 |

The brand campaigns in the Netherlands and Belgium significantly contributed to a higher reputation score. Both policyholders and non-policyholders perceive DELA as reliable, successful and socially responsible. We saw an increase in our reputation in Belgium due in part to further optimised customer communication, the implementation of a new CRM system and improvements to our website. Specific reputation measurements are not yet conducted in Germany. As a newly established organisation in Germany, our focus is on building our core activities and infrastructure. As we grow, we will begin measuring our reputation and closely monitor and evaluate the results.

Employees

Employees are crucial to the service provided to our policyholders. As part of good employment practices, we invest in our employees to ensure they are engaged, proud and fit, and have room for personal development.

DELA Natura had 762 employees (670 FTE) at the end of the year, the majority of whom are based in the Netherlands.

| Male | Non-binary | Female | Male | Non-binary | Female | |

|---|---|---|---|---|---|---|

| Netherlands | 241 | 360 | 601 | 225 | 288 | 513 |

| Belgium | 39 | 65 | 104 | 39 | 64 | 103 |

| Germany | 28 | 29 | 57 | 27 | 26 | 54 |

| Total | 308 | 454 | 762 | 291 | 379 | 670 |

We consider the Employee Net Promoter Score (eNPS) to be the key indicator for the well-being of our employees and the degree of impact, both positive and negative. Employee satisfaction is measured annually among permanent employees in the Netherlands, Belgium and Germany using the employee satisfaction survey from Effectory.

The eNPS for Natura shows that employee satisfaction remains high at 43 points. Unfortunately, we did see a decline. The measures introduced in early 2024 to improve on the results of the 2023 survey were only implemented in the second half of 2024, too late to make a positive contribution to this year's eNPS. The measures will remain in place in 2025 and be supplemented with department- and team-specific actions to further increase satisfaction levels.

Just like last year, DELA has been named a ‘World-class Workplace’ in Belgium by Effectory. Organisations receive this label when they score above the benchmark average on eNPS and employer engagement.

In Germany, the eNPS has increased by 2 points. This is a good result for a standalone business unit that is building its position in the German market.

| 2024 | difference | 2023 | |

|---|---|---|---|

| Effectory eNPS | |||

| Netherlands | 44 | -3 | 47 |

| Belgium | 54 | -3 | 57 |

| Germany | 10 | +2 | 8 |

| Total | 43 | -3 | 46 |

We encourage employees to bring out the best in themselves every day through team plans and personal development plans. A targeted range of training sessions and workshops support this and we also link learning opportunities to our organisational goals. In 2024, at least 75% of permanent employees had a personal development plan.

We also find it important that the workforce reflects society as much as possible, ensuring everyone has equal opportunities and feels safe to be themselves. However, DELA has yet to implement specific policies, targets or actions to eliminate discrimination, stimulate equal opportunities, and promote diversity, equity and inclusion. This plan is currently being developed and expected to be finalised in 2025.

A dialogue session was organised in the Netherlands in 2024 to raise awareness around discrimination and inclusion among employees and managers. In 2025, a working group will be set up with interested employees to build support for the diversity policy.

Absenteeism

We believe it is important that every employee is physically and mentally healthy and able to perform their work well, both now and in the future. The absenteeism rate for DELA Natura employees in 2024 due to illness, personal circumstances and other causes was 4.0% in the Netherlands (2023: 3.9%), 6.6% in Belgium (2023: 5.4%) and 6.5% in Germany (2023: 6.7%). Absenteeism continues to require extra effort from our advisors (particularly in the areas of prevention, occupational health and well-being) and HR business partners.

To reduce absenteeism, we pay a lot of attention to the personal responsibility model and various preventive initiatives are underway. We continuously invest in safety measures and health programmes, ensuring that employees feel valued and protected. This includes training in areas such as physical strain and dealing with inappropriate behaviour such as aggression.

For Belgium, a ‘Safety and Health Policy Plan 2023 – 2028’ is in place. Along with its associated measures, this plan has been communicated to employees and is available for reference on the intranet. Topics such as the prevention of workplace accidents, fire safety, ergonomics and managing psychosocial work stress are included. The plan also provides for regular training sessions and includes periodic inspections. Reports on these activities are regularly shared with the committee for prevention and protection at work (CPBW).

In addition, attention is paid to ergonomics to prevent physical strain. We also strive to prevent workplace accidents by ensuring that all incidents, whether large or small, as well as hazardous situations, are reported through our personnel system, safety advisors, HR business partners, trusted contacts, managers or anonymously via whistleblower software, in order to take appropriate action.

Turnover

The turnover rate compared to the average number of Natura employees was 10 percent over the past year. Employee turnover remains a regular topic on the agenda of the various management teams.

To consider the well-being of employees from the outset, we take into account the different wishes and needs of various target groups in our recruitment campaigns. The information is based on data we have gathered over the past two years, as well as feedback received from current and former employees.

Business operations

Various strategic and operational activities and decisions form the foundation for an efficient, transparent and future-oriented organisation. This year saw us take significant steps to optimise and streamline our internal processes. Clear guidelines, concrete control programmes and a consistent architecture aim to generate synergy effects. We then leverage on these synergies to enhance collaboration, drive innovation and achieve sustainable growth, ensuring that our organisation remains flexible and adaptable.

IT architecture and governance

In 2024, we defined and successfully delivered the group’s target architecture and roadmap. We also initiated a mapping of the current IT organisation’s operating model. This analysis provides the foundation for potential adjustments to the operating model, both at the group level and within individual countries.

Governance has also been strengthened to enable a more effective management and cost control.

Finally, we conducted an assessment of the impact of inter-company IT service provision on taxation, legal and compliance aspects. The findings will be used in early 2025 to develop an action plan, which will also take into account the new management structure.

Control programmes

Business in control

In 2025 we will continue to implement ‘Business in Control’, which started out as a separate programme but is now firmly embedded in our daily processes. We have trained teams and clearly defined roles & responsibilities, incorporating risk-awareness as a fixed value in our decision-making.

As part of the risk assessment process, we actively examined tolerances for acceptable risks. This process was not only documented but practically tested within various business operations.

After previously using different standards, we have now aligned our risk taxonomy with the Operational Risk Exchange (ORX) standard. This process provides a solid foundation for risk analysis and reporting. Adopting a single uniform standard improves data comparability and aligns with best practice.

Digital transition of insurance chain and other insurance projects

The Dutch multi-year digital transition programme aims to replace the administration systems of our insurance portfolio. This large-scale programme has faced several challenges in recent years. A more simplified approach was adopted in 2024, focusing on the standardisation of insurance processes to create a future-proof system and prepare for the migration of one product group. A phased plan will be developed in 2025 in parallel with the migration of the remaining products and potential implementation scenarios for Belgium will be explored. This phased approach is enabling us to continue building a future-proof administration platform, integrated with the personal online environment MijnDELA to ensure members have control over and access to their data.

Efforts have been made in both the Netherlands and Belgium to enhance customer experiences in relation to taking out and paying for insurance. In the Netherlands, the online insurance application process has been simplified, while a new CRM system was introduced in Belgium to support customer communication. Moreover, premium invoices in Belgium are now sent via the POM platform (https://www.pom.be/nl). This enables invoices to be delivered both on paper and digitally, with payment options available through Payconiq, featuring a payment button or QR code for added convenience.

DORA

As part of the Digital Operational Resilience Act (DORA), significant progress was made in 2024 to comply with the additional requirements in ICT risk management, incident reporting and cyber resilience. This regulation has been integrated into our supplier contracts, ensuring clear agreements on security and resilience. It will also lead to optimised IT core processes and improved role clarity within our organisation.

Digital Finance

Digital Finance is a group-wide programme aimed at replacing outdated financial administration software and providing the Belgian and Dutch entities with a modern and future-proof system. Various interfaces for communication with other systems have also been developed and continue to be implemented. Following the general system setup, a phased rollout began in Germany and Belgium, starting with Belgian crematoriums. Additional entities, including Funerals Assistance and Real Estate, are scheduled to be integrated into the new system during 2025.

Finances

Our focus is on certainty, care and continuity rather than maximising profits. The goal is to ensure policyholders can face the future with as few concerns as possible and a stable pay-out based on a premium that is kept as low as possible. We aim for an optimum balance between investments, profit sharing and solvency.

Premium Income

After deducting the reinsurance premium, total premium income in 2024 was €743.9 million (2023: €712.7 million), a 4% rise compared to the previous year (2023: 7%).

In the Netherlands, premium income rose by €11.4 million to €492.1 million, primarily due to the premium increase for the DELA Uitvaartplan effective on 1 January 2024. In Belgium, premium income was €173.1 million (2023: €161.9 million), reflecting a growth of nearly 7% that was driven by a steadily expanding portfolio. Premium income increased in Germany by over 12% in 2024 to €78.7 million (2023: €70.1 million). As in Belgium, this growth was also attributed to an expanding portfolio.

Income from premiums after deducting reinsurance premium:

| Amounts x €1,000 | 2024 | difference | 2023 |

|---|---|---|---|

| Netherlands | 492,148 | +11,399 | 480,749 |

| Belgium | 173,130 | +11,241 | 161,889 |

| Germany | 78,663 | +8,600 | 70,063 |

| Total | 743,941 | +31,240 | 712,701 |

Operating result

The operating result is the result achieved from our core activity insurance, excluding extraordinary gains and losses, profit-sharing and taxes. DELA Natura's operational result for 2024 is €80.6 million – a six percent increase compared to 2023.

| Amounts x €1,000 | 2024 | difference | 2023 |

|---|---|---|---|

| Premium income | 743,941 | 4% | 712,701 |

| Interest accrued from technical provision | 204,959 | 8% | 189,851 |

| Underwriting costs | -682,194 | 4% | -657,284 |

| Technical margin | 266,706 | 9% | 245,268 |

| Operating expenses* | -165,821 | 12% | -148,551 |

| Acquisition costs* | -20,247 | -2% | -20,608 |

| Operating result | 80,638 | 6% | 76,108 |

Investment result

The net investment return over 2024 was 6.8% positive (2023: 4.6% positive). The return on equities was approximately 17.3% and on fixed-income securities 4.2%. Real estate investments yielded a return of 2.1%. The return on infrastructure investments was 4.3%, with agriculture & forestry investments yielding 4.4%. The net investment result in 2024 amounted to €578 million (2023: €337 million).

The volatility in the value of investments is a direct consequence of our strategic investment choices. These are aimed at achieving solid long-term returns, on which our premium is based, as well as to outpace any rise in funeral costs. The nature of our insurance policies (which are in most cases paid out upon death) translates into long-term obligations. Investment results can fluctuate as this extended horizon makes an offensive strategy possible. By accepting a calculated risk in our investment strategy, we have been able to achieve the required results over the years. A consequence of this policy is that there are sometimes significant fluctuations in the value of our investment portfolio.

Development of technical provisions

The technical provisions, including a provision for profit-sharing and minus deferred acquisition costs and reinsurance, increased by €558.8 million. The technical provisions on our balance sheet are based on fixed principles such as the actuarial interest. As a result, the impact of higher or lower interest rates and/or inflation is not visible on this balance sheet provision. On the basis of market value, the technical provisions increased by €737.8 million. This difference of €179.0 million is also shown in the reduction of the surplus value of the liability adequacy test on the technical provisions.

Coverage ratio

The coverage ratio represents the market value of investments as a percentage of the market value of guaranteed liabilities and is influenced by factors such as interest rates, mortality and costs. The coverage ratio at the beginning of the reporting year was 219%, ending at 200%.

In 2024, interest rates and inflation decreased slightly, which led to a 7 percentage points decline in the coverage ratio. Due to developments in the insurance portfolios, the coverage ratio dropped by 4 percentage points. Higher expected future costs resulted in a 5 percentage point decrease. Other developments (model changes and updating of actuarial assumptions) led to an 11 percentage point decline in the coverage ratio. Investment returns resulted in an 8 percentage point increase.

| Start of year | Dampening effect | Enhancing effect |

Year-end | |

|---|---|---|---|---|

| Start of year | 219% | |||

| Lower interest rate and inflation | -7% | |||

| Increase in expected costs | -5% | |||

| -12% | ||||

| Developments in insurance portfolio | -4% | |||

| Investment result | 8% | |||

| Other factors | -11% | |||

| -7% | ||||

| Year-end | 200% |

Profit sharing

In 2024, profit-sharing was determined at €281.2 million (2023: €249.2 million). Funeral costs rose by 5.84% (2023: 6.62%). The average coverage ratio remained high, which enabled us to realise a 100% profit share for DELA UitvaartPlan policyholders in the Netherlands. Profit-sharing was also high for policyholders of the funeral product in Belgium. All in all, these results were again very positive for our policyholders.

| Amounts x €1,000 | 2024 | 2023 | 2022 | 2021 | 2020 |

|---|---|---|---|---|---|

| Granted | 281,247 | 249,224 | 43,654 | 5,940 | 42,994 |

Premium adjustment

Some 55 percent of insurance customers have the DELA UitvaartPlan policy, the premium for which in the Netherlands rose on 1 January 2025 by 5.84 percent (1 January 2024: 7.57 percent). This rise was related in principle to three factors: inflation, allocated profit sharing and the possible premium measure:

- 5.84% increase related to rising funeral costs. This component of the premium change is determined annually by the general meeting. The expected inflation rate for the following year determines the proposal for the premium increase as of 1 January. The expected inflation was 5.84 percent, and this figure was proposed to and adopted by the general meeting as the component for the premium adjustment on 1 January 2025.

- 0.00% increase related to not fully awarding profit distribution for the coverage of the back-service. The total premium for the back-service amounts to 4.44 percent, with 100 percent allocated as a profit-sharing percentage. As a result, no back-service costs were passed on to policyholders.

- 0.00% increase related to the premium measure due to structurally low interest rates and a low coverage ratio. Since the average coverage ratio in 2023 was above 120 percent, no premium measure was required.

Solvency ratio

DELA determines its solvency in accordance with the Solvency II risk-based capital regime, hence the name Solvency II ratio. This European calculation framework takes into account the risks included in the balance sheet of the insurer when determining solvency. The Solvency II directive requires sufficient solvency as a precondition for profit-sharing.

The solvency ratio fell from 207% to 201% at the end of the year but remains robust. Due to developments in investment returns, the asset mix, interest rates, inflation and volatilities, the Solvency II ratio dropped by 14 percentage points. Adjustments to actuarial parameters led to a decrease of 5 percentage points. Developments in the insurance portfolio during 2024 resulted in an increase of 12 percentage points, with other developments leading to a 1 percentage point increase.

| Start of year | Dampening effect | Enhancing effect |

Year-end | |

|---|---|---|---|---|

| Start of year | 207% | |||

| Change to the economic parameters (interest, inflation, volatility), asset mix and investment results | -14% | |||

| Changes to actuarial paramenters | -5% | |||

| -19% | ||||

| Development of insurance portfolio | 12% | |||

| Other developments | 1% | |||

| 13% | ||||

| Year-end | 201% |

Sustainability

As a public interest entity, DELA Natura acknowledges its responsibility to contribute to a sustainable future. We are exempt from specific sustainability reporting as all relevant information can be found in the sustainability statement issued by DELA Coöperatie UA in Eindhoven (jaarverslag2024.dela.nl).

This statement is the first to be issued under the guidelines of the Corporate Sustainability Reporting Directive (CSRD). Effective from the 2024 financial year, this regulatory framework was established by the EU to improve and standardise sustainability reporting among companies.

Governance

Governance

Corporate governance at DELA stands for prudent management, good oversight and transparent accountability. We focus on the long-term interests of our members: costs and risks are carefully monitored and opportunities identified. The strength of DELA lies in its entrepreneurship and flexibility to address risks and seize opportunities. We do this with a clear ambition that is based on our core values, ensuring the quality of ethical business operations and the principles of a learning organisation.

Corporate governance

Governance charter

The governance structure is detailed in a governance charter. This ensures that we comply with decrees and regulations based on European legislation such as Solvency II, the General Data Protection Regulation, the Digital Operational Resilience Act (DORA) and the Corporate Sustainability Reporting Directive (CSRD), along with national legislation and regulations like the Dutch Financial Supervision Act, policy regulations and best practices from regulators and the Code of Conduct for Insurers. Our company culture is another major component of this. We regularly evaluate the governance charter and will adjust it in 2025 based on our new management structure, taking the group executive board structure as a starting point.

Legal structure

DELA Coöperatie UA (hereafter: 'DELA’) is a cooperative for members with the following purposes:

- to help its members by serving their interests;

- ensuring policyholders and co-insured a dignified and affordable funeral;

- to improve the reputation of the life insurance market and the funeral sector.

DELA includes DELA Holding NV and Voor Elkaar Holding NV. The Executive Board of the cooperative governs these two entities.

DELA Holding NV includes three principal companies: DELA Natura- en levensverzekeringen NV (hereafter: DELA Natura), DELA Uitvaartverzorging NV and DELA Holding Belgium NV.

DELA Natura accommodates all Dutch, Belgian and German insurance activities. The Belgian and German activities are carried out via a branch office of the Dutch insurance company.

The principal companies include subsidiaries and participations. DELA Holding NV always governs the principal companies. Each principal company governs its subsidiaries. In addition, each company may have a director. The authority of each director is defined per company in its statutes, in the authorisation regulations for the relevant company segment and in the Chamber of Commerce registrations.

Permits and supervision

DELA Natura is supervised by The Netherlands Authority for Financial Markets (AFM) and Dutch central bank (DNB), and is registered under licence number 12000437. The Chamber of Commerce registration number of DELA Natura is 17078393.

DELA Belgium carries out insurance activities which are accommodated by the Dutch company DELA Natura, and funeral activities that are part of Belgian companies. Other activities in Belgium take place within the entity DELA Enterprises NV. The insurance activities are carried out under the licence issued by DNB and prudential supervision activities are also overseen in Belgium by DNB. With regard to the supervision of conduct, DELA Belgium is accountable to the Belgian Financial Services and Markets Authority (FSMA). DELA’s registration number at the Chamber of Commerce is 17012026.

The insurance activities in Germany take place via a branch office in Düsseldorf (article 2:115 Dutch Financial Supervision Act), with an emphasis on marketing and sales. Other financial and actuarial activities are carried out at the head office of DELA Natura in Eindhoven. The insurance activities and prudential supervision in Germany come under the license issued by DNB with supervision of conduct provided by the Bundesanstalt für Finanzdienstleistungsaufsicht.

Supervisory Board

The Supervisory Board consists of at least five and at most seven natural persons as determined by this Board. At this moment, there are 6 members. If possible, two members will also be (replacement) members of the general meeting. The composition of the Supervisory Board is such that the combination of experience, expertise and independence of its members meets the Supervisory Board profile and allows it to perform its various duties. The members are appointed by the general meeting based on the suggestion of the Supervisory Board.

The tasks and duties of the Supervisory Board include overseeing, monitoring and providing advice to the Management Board on:

- realisation of the goals of the cooperative;

- the strategy and risks related to its activities;

- the setup and functioning of internal risk management and control systems;

- the financial reporting process;

- compliance with legislation, regulations and the risk policy;

In addition, the Supervisory Board is responsible for:

- compliance with and enforcement of the corporate governance structure;

- approving the financial statements, budget and material capital investments;

- selecting and appointing the external accountant;

- approving the risk tolerance;

- nominating members of the Management Board for appointment and resignation;

- determining the remuneration policy.

The Supervisory Board evaluates the remuneration policy and the functioning of the Management Board. The chair is the point of contact for any alleged irregularities regarding the functioning of Management Board members. In fulfilling its duties, Supervisory Board members focus on the interests of the cooperative and its associated companies. They carefully consider the interests of the various stakeholders of the cooperative in doing so, including members and employees. The Supervisory Board itself is responsible for the quality of its own functioning.

Regulations

The Supervisory Board has internal regulations that provide rules for its decision-making process. The regulations are drawn up by the Supervisory Board and adopted by the general meeting. They serve as a supplement to the regulations and guidelines that apply to the Supervisory Board based on Dutch legislation and the cooperative’s statutes.

Appointment and term

Each Supervisory Board member is appointed for a period of up to four years and can be re-appointed twice. The final four-year term will consist of two two-year periods with an interim evaluation. A member will step down at the latest after the first general meeting held after four years have passed since their last appointment. A member who is stepping down can be reappointed immediately, insofar as the maximum term of 12 years is not exceeded.

Committees

The Supervisory Board has an audit committee, risk committee and a remuneration and appointment committee.

Participations

The members of the DELA Supervisory Board are also appointed as Supervisory Board members for DELA Holding NV and DELA Natura. The establishment of a Supervisory Board for DELA Natura was compulsory to meet the requirements of the Dutch Financial Supervision Act.

Personal details of the Supervisory Board

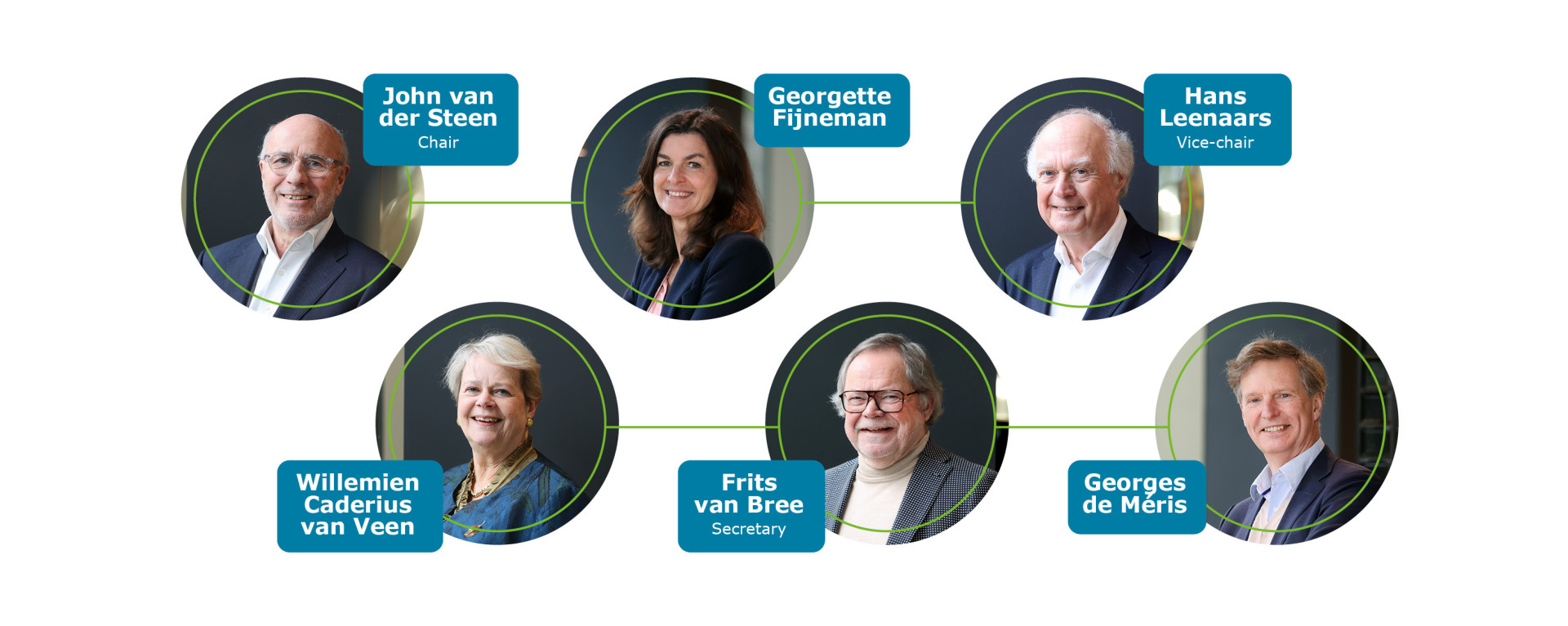

The Supervisory Board has six members. All are part of the Supervisory Board of DELA Coöperatie UA, DELA Holding NV and DELA Natura- en levensverzekeringen NV.

J.W.Th. (John) van der Steen (1954), chair

- Male, Dutch citizen.

- Appointed in 2019, currently serving second term.

- Function: professional supervisor, DGA Ansteen Holding BV.

- Other additional functions: chair of Supervisory Board of BinckBank NV, chair of Supervisory Board of Princess Sportsgear & Traveller BV, member of the Executive Board of Stadhold (Randstad) Insurances SA and Stadhold Reinsurances SA, member of Executive Board of Vereniging AEGON, Ambassador for Royal Concertgebouw Orchestra.

J.J.A. (Hans) Leenaars RA (1952), vice-chair

- Male, Dutch citizen.

- Appointed in 2015. Currently in third term.

- Position: professional supervisor.

- Additional functions: member of Executive Board of Stichting John van Geunsfonds, chair of Supervisory Board of Stichting Het Klooster Breda, chair of Executive Board of Stichting Via Nobel, Chair of Advisory Board of ILFA BV.

G.C.A.M. (Frits) van Bree RA (1952), secretary

- Male, Dutch citizen.

- Appointed in 2021 by members of the general meeting, currently in first term.

- Position: professional supervisor.

- Additional functions: council member of Vereniging Eigen Huis.

W.A.P.J. (Willemien) Caderius van Veen RA (1959)

- Female, Dutch citizen.

- Appointed in 2014 and now in third term.

- Position: professional supervisor, DGA Caadje BV.

- Additional functions: member of Supervisory Board of Unilever Nederland Holdings BV, chair of the Review Committee Pensioenfonds Lloyds Register Nederland, member of Supervisory Board of Woningcorporatie Trivire, member of Supervisory Board of Ondernemingspensioenfonds Capgemini, member of Supervisory Board of the Dutch foundation for liver and gastrointestinal research (SLO) at EMC Rotterdam, chair of STOER foundation in Rotterdam.

G.M. (Georgette) Fijneman (1966)

- Female, Dutch citizen.

- Appointed in 2022, currently in first term.

- Position: chair of Executive Board of health insurance company Zilveren Kruis.

- Additional functions: vice-chair of Zorgverzekeraars Nederland, Executive Board member of Kansfonds, Ambassador for Nederlandse straatdoktersgroep (unpiad).

G.H.C. (Georges) de Méris FCA (1961)

- Male, Dutch citizen.

- Appointed in 2019 by members of the general meeting, currently serving second term.

- Position: Executive Board member and professional supervisor.

- Additional functions: chair of Executive Board of Stichting AK Stop Diabetes Invest, member of Supervisory Board of Omroep Brabant, chair of Supervisory Board of Hy2Care BV, chair of Supervisory Board of Caelus BV, chair of Supervisory Board of Matisse BV, board member at Stichting SFO.

Management Board

DELA Natura has a Management Board consisting of a number of natural persons determined by the Supervisory Board. Jon van Dijk was a member of the board until his retirement in July 2024 after which he was succeeded by Godelieve van Velsen. Jack van der Putten resigned as director in 2025 en is opgevolgd door mevrouw S.M.G. Schellekens - Lyppens. The board is responsible for managing the company and overseeing its assets, except for the restrictions in the statutes. It can determine which specific task each director is assigned, the division of which must be approved by the Supervisory Board.

Personal details of the Management Board

Drs. S.M.G. (Sandra) Schellekens – Lyppens (1965), director

- Female, Dutch citizen.

- Position in the DELA Group: CEO, chair of Executive Board (since 27 January 2024).

- Focal areas: human resources, internal audit, compliance, branding, administrative affairs, DELA Netherlands and DELA Belgium (until 1 March 2025).

- Also Managing Director of DELA Netherlands since 27 January 2024.

- Appointment period: four years, starting on 27 January 2024.

- Additional functions: Supervisory director at Rabobank Regio Eindhoven and ZLM Verzekeringen.

Drs. G (Godelieve) van Velsen RA (1969), director

- Female, Dutch citizen.

- Position in the DELA Group: CFRO (since 1 July 2024).

- Focal areas: actuarial affairs, finance, investments, risk management, CSRD, tax and DELA Germany (until 1 March 2025).

- CFO DELA Netherlands since 1 juli 2021 .

- Appointment period: four years, starting on 1 July 2024.

- Additional functions: none.

Investments

The Asset Management department in the Netherlands conducts the investment activities. DELA Natura has an investment advisory committee (BAC) which has an advisory role to the Management Board on investments. In addition, it is asked for advice regarding policy proposals, policy changes and the implementation of policy in this field. If the committee’s advice is rejected by the Management Board, the Management Board must report this to the Supervisory Board. The investment advisory committee has an explicit advisory role and evaluates whether proposals are consistent, comprehensive and sound with regard to return, risk and sustainability. The Management and Supervisory Board maintain their own responsibilities. The investment advisory committee is composed of at least three external members who are appointed by the Supervisory Board as proposed by the Management Board.

Risk management

As DELA Natura our Risk management makes a direct contribution to long-term goals and provides an insight into the sensitivities and correlations of strategic, financial, operational and compliance risks to ensure that we can effectively address developments and take timely action to realise our goals and secure continuity of the organisation.

In practice

DELA applies the ‘three lines’ model for the setup of the management and control of risks:

- The first line is primarily responsible for realising the formulated goals of the company and the demonstrable realisation of internal control measures and effective risk management. Responsibilities of the first line include the operations, results, definition of risk appetite, management and compliance with internal control measures;

- The second line provides advice, coordinates, safeguards and evaluates – independently from the first line – whether or not the first line is actually taking responsibility and operating within the risk tolerance of DELA;

- The third line ensures additional assurance of the quality of internal control via audits.

The independence of the second and third lines is an important starting point to ensure this model functions properly, which is why it is safeguarded. The overview below shows a schematic representation of the model.

Process

We follow a process for risk management that ensures insight into the main risks and opportunities in all circumstances. Opportunities, risks and applicable control measures are always carefully weighed. The Operational and Compliance Risk Management department facilitates the risk management process.

Identifying risks

Risk identification is primarily the responsibility of the first line. The second line periodically analyses the risks identified by the first line and supplements them where necessary, with a special focus on potential risks. This analysis is then discussed in meetings between the second and third line.

Below is a summarised risk profile for DELA. Further details of the risk categories included can be found in the risk section of the financial statements.

The figure above shows which risks are deemed important or less important. The overview is based on an estimate of the probability that a specific risk might occur combined with an estimate of the impact if that should be the case, taking into account the measures needed to limit the probability and/or impact.

Defining risk appetite and limits

The Management Board evaluates the risk profile annually based on predetermined operational goals and the capacity of the organisation. In addition, the Board determines the risks DELA as an organisation is prepared to take – based on its risk profile – to achieve its strategic goals, in line with its risk appetite. In addition to the intended goals, it is essential that the continuity of the organisation is secured. The risk appetite consists of the risk appetite statements and the declarations on quality and quantity. These are translated into risk limits and risk tolerances to enable continuous monitoring and control. The table below shows the risk appetite for the main risk categories, with financial risks at the aggregated level.

With regards to strategic and financial risks, we are willing to accept uncertainty – as part of our business model – even when the potential benefits are uncertain. We apply a defensive attitude for integrity risks and aim to run few risks in this area. Our appetite for operational risks falls in between the two. A detailed explanation of the risk categories we apply and the underlying risks is included in the financial statements.

Managing risks

Risk mitigation solutions are applied to ensure the risks remain within the desired bandwidths. In most situations this involves a suitable mix of:

- terminating or outsourcing activities;

- reducing risks by applying preventative measures;

- transferring risks via (re)insurance and/or the application of contract management;

- accepting risks that can be carried by the organisation itself.

If risks are outside of the predetermined risk limits – and therefore greater than desired – management will take additional mitigation measures. The deliberate breach of risk limits is only allowed with approval from the Management Board, and only when of a temporary nature. The risk appetite statements will be evaluated and optimised in the beginning of 2025. Our risk appetite regarding these risks did not change in 2024.

Monitoring and reporting

Monitoring and evaluating risks and the risk management system are important preconditions for the type of learning organisation that we aim to be.

In assessing a risk an evaluation is made of whether it remains within the risk appetite level. The starting point is that risks exceeding the appetite are reduced to a lower risk level based on a good mix of risk mitigation solutions.

To ensure constant risk monitoring, management determines KRIs (key risk indicators) for each risk within the risk profile, monitors the development of these indicators at least once per quarter, and evaluates the extent to which risk limits and tolerances are exceeded. Extra management actions are defined when breaches occur. In addition, the second and third line periodically report to the Management Board.

Management periodically participates in a Risk Control Self Assessment (RCSA) process which results in a Control Statement (ICS). In addition, the Internal Audit department evaluates the setup and effectiveness of the risk management system.

Own Risk and Solvency Assessment

Solvency II requires a demonstrably balanced weighing up of risk management, capital management and the corporate strategy. The Own Risk and Solvency Assessment (ORSA) is the process structure for this assessment and the degree of compliance is shown in the ORSA report. The content of the scenarios and stress scenarios is determined by the Management Board before the ORSA starts, after obtaining advice from the second line.

Management uses the ORSA at least once a year or when developments occur that may significantly affect the risk profile. This helps determine whether the risk profile is still appropriate in light of the company goals, risk appetite and available capital buffers. Various (stress) scenarios are taken into account in this process.

The results of the ORSA 2024 show that DELA’s solvency position is robust. This year’s OSRA shows a gradual increase in the coverage ratio of the basic scenario. Policyholders can therefore expect a significant profit share depending on their type of policy, while premium increases remain limited. We have no influence on interest rates or inflation curves, but can have some impact on the amount of funeral costs. The ORSA 2024 has again shown that scenarios with low funeral cost inflation (combined with low interest rates) can put pressure on the solvency and/or premium increase.

Capital management

Capital policy is aimed at maintaining a solid solvency position, in which we are constantly looking for a good balance between the amount of capital (assets) we maintain and the risks we face. In this framework, we have defined an internal minimum solvency capital requirement which we always aim to exceed. The requirement value for each licensed entity (DELA Cooperative and DELA Natura) has been established at 150 percent.

The capital policy defines various actions should the solvency ratio drop below the internal minimum solvency capital requirement. The solvency ratio was constantly higher than the solvency requirement during 2024.

For more details on risks and how they are managed please refer to the financial statements: ‘financial statements’, ‘Notes on the balance sheet and income statement’, ‘3. Risk’.

Developments in 2024

While their management is a continuous process, risks do sometimes occur nonetheless. In this section we examine the risks faced in 2024 and the measures taken to minimise the chance and/or impact thereof. We also present some of the general measures taken to limit risks.

Strategic risks

Stress tests show that while our solvency position is robust, we are sensitive to scenarios with a low interest rate and low inflation. Preparatory measures are taken or different choices made where necessary. The main preconditions and measures are developed in the capital policy, which is evaluated annually. The risks are therefore considered limited and no additional capital has to be set aside. Stress tests were also performed with a focus on the impact of climate change. The conclusion to date is that our financial position is only slightly financially susceptible to this risk based on the current expectations. In 2024, there were several (group) Executive Board changes. In the fourth quarter, we began drafting a new long-term business plan (2026-2030), which will be further developed in 2025. Long-term risks have been identified, focusing on financial robustness and, where necessary, measures have been proposed to mitigate them. We are also examining how our organisational structure and risk management organisation can best support these risks.

Integrity risks

Not complying with legislation and regulations is a risk that can harm our continuity and reputation. There were no serious incidents in this field in 2024. To further manage such risks, we worked hard in 2024 on professionalising the procurement and outsourcing policy, having compliance with the applicable sanctions legislation and regulations as a precondition. Our policy was tested against standards such as DNB’s 'Good practice document for outsourcing by insurance companies’. In addition, we found options for improvement in how we handle the limited risk of conflicts of interest in sponsorship agreements. These improvements will be implemented in 2024.

Operational risks

Operational risks are caused by external influences, human error and the failure of processes and systems. Despite clear processes, responsibilities and reporting, these risks can never be fully excluded and it is important to learn from the past to prevent repeats in the future. The nature and scope of these incidents is very diverse and varies from several (attempted) cases of fraud and cyber-attacks to operational incidents in our funeral centres such as occupational accidents and errors related to cremations.

All these incidents have been assessed and, where necessary, extra measures taken such as improving instructions and/or tightening up protocols. We specifically focused on the throughput times of various steps in the process.

Internal control

In 2024, we continued the ‘Business in Control’ programme aimed at enhancing internal control and reducing operational and compliance risks. The objective of this programme is to improve and further standardise the maturity of risk management for operational and compliance risks. We also focused on implementing Governance, Risk and Compliance tooling in the Netherlands and evaluating the risk management system. The focus in 2025 will shift to further implementation and the rollout of the programme in Belgium and Germany.

DORA

The Digital Operational Resilience Act (DORA) is a European directive designed to help financial organisations better manage IT risks and become more resilient to cyber threats. In 2024, we focused on implementing the requirements stemming from DORA to ensure timely compliance with this regulation.

Digital transition

IT systems that are not future-proof are a major risk that could endanger the continuity of DELA and the quality of our service provision to customers. We are active in (preparing) the replacement of various IT systems. Administrative systems are being systematically replaced or optimised to enhance the customer experience and improve our service delivery. Outdated systems are being phased out to keep costs for members as low as possible.

Financial risks

The financial markets are a source of risk. Interest rate developments not only affected the solvency position and coverage ratio, but also the results of our investment portfolio. The increased interest rate also leads to refinancing risks in the real asset portfolio. The results of an ALM study conducted in 2024 led to a minor adjustment in our strategic asset allocation, with a slight increase in the strategic allocation to infrastructure at the expense of real estate and shares.

A further clarification on the development of the financial risks (including the associated quantification) is included in the risk section of the financial statements.

Outlook

Outlook

We have a rich history and a future focused on growth, where connections, innovations, synergies and continuous learning play a crucial role.

The long-term strategy (2026-2030) for DELA Group will be established in 2025 and the management structure aligned to this as an extension of that mentioned under 'Governance.' while this will also serve as the starting point for DELA Natura, there are several areas on which we will specifically focus.

Strengthening connections

The cooperative model is under pressure as individualisation increases. We are therefore aiming to deepen our relationship with policy holders by offering greater support. High customer satisfaction remains one of our top priorities. By actively working towards a consistent service standard, we ensure that policy holders continuously experience the same high level of quality. This is what we stand for.

We are also enhancing our preferred position by further optimising our services. This includes the development of new products and services that align with our core activities. For example, we continue to develop (new) insurance packages that cater to the specific needs of different target groups.

Growth

We aim to achieve healthy growth and specifically a net growth in policyholders. At the same time, we recognise a declining willingness to purchase insurance policies in general. Wishing to help more people with financial support related to 'passing on and remembrance', we are therefore striving to raise awareness of our products and services among a broader audience.

In Belgium we are aiming to personalise our services both in terms of communication and with various tools and systems. In Germany, we are learning from the existing structures in the Netherlands and Belgium as an insurer. The integration of German quality standards such as Bipro certification enables us to further expand our position in the broker segment. We are also preparing to develop the direct-to-consumer sales channel.

Building our brand and reputation

The distinctiveness and social engagement of our brand are becoming increasingly important. In Belgium and the Netherlands, we continue to launch and develop corporate campaigns to support the DELA brand and reputation. These campaigns appear on television, radio and social media, where we present ourselves as a trusted funeral insurer.

Good employment practices

Our employees interact daily with our policy holders, and in doing so make the difference. Good employment practices are therefore of critical importance. Specific action plans address challenges related to employee satisfaction, absenteeism, staff turnover and labour market shortages. We also focus on personal development opportunities and continuously promote our core values of engagement, integrity and entrepreneurship. The ultimate objective is to enhance employee satisfaction.

We value a workforce that reflects society, where everyone has equal opportunities and feels safe to be themselves. DELA is actively developing a plan to promote diversity, equality and inclusion, which is set to be finalised in 2025.

Sustainable and flexible organisation

As an organisation, we strive for continuous improvement and are committed to building a sustainable and flexible company. Learning and collaboration are central to this approach. The current European regulations, which apply to all countries in which we operate, help us professionalise our processes and accelerate progress. This includes projects such as DORA and sanctions legislation. Market developments are evolving rapidly and digitisation is now a permanent factor.

The ‘Business in Control’ programme, aimed at enhancing operational and compliance risk management, has been partially implemented to ensure critical business processes are well-managed. We will continue with this implementation during 2025. Furthermore, our products and services require a solid digital foundation that supports personal choices while remaining efficient and flexible. We are working on a digital strategy and IT roadmap that will be rolled out in each country. Examples of strategic IT programmes include the digital transition programme in the Netherlands and ‘Digital Finance’, which focuses on replacing financial applications. Generic IT services and administrative systems are being implemented across all three countries wherever possible and, here too, optimising the customer experience remains a key focus.

We are also furthering our sustainability efforts by implementing and expanding the climate transition plan, with additional activities to reduce Scope 3 CO2 emissions.

Solid financial basis

A firm financial foundation is essential for the continuity of the cooperative. Our policyholders should be able to look to the future with as much confidence as possible, supported by an inflation-proof funeral insurance policy at the lowest possible premium. Careful asset management plays a key role in this. The year 2025 began with significant turmoil in the financial markets, and we expect this uncertainty to persist for the time being. In these turbulent conditions, we continue to adhere to our carefully constructed investment policy, which is focused on the very long term. By broadly diversifying our investments, we aim to absorb market fluctuations as effectively as possible and focus on minimising risks. We closely monitor developments in the markets and, when necessary, implement measures that always take into account long-term sustainable value creation.

In addition, we continue to carefully manage costs, especially given the current inflation levels. Synergies are achieved by optimising learning across the group and enhancing collaboration.

We would like to conclude by thanking our employees and partners for their dedication and express our confidence that together we can provide financial peace of mind for policy holders. We look to the future with confidence.

Eindhoven, 7 May 2025

Sandra Schellekens - Lyppens

Godelieve van Velsen